UK build to rent has made huge progress over the past decade, becoming less of a ‘niche’ area and more a mainstream development strategy to plug the rental supply gap.

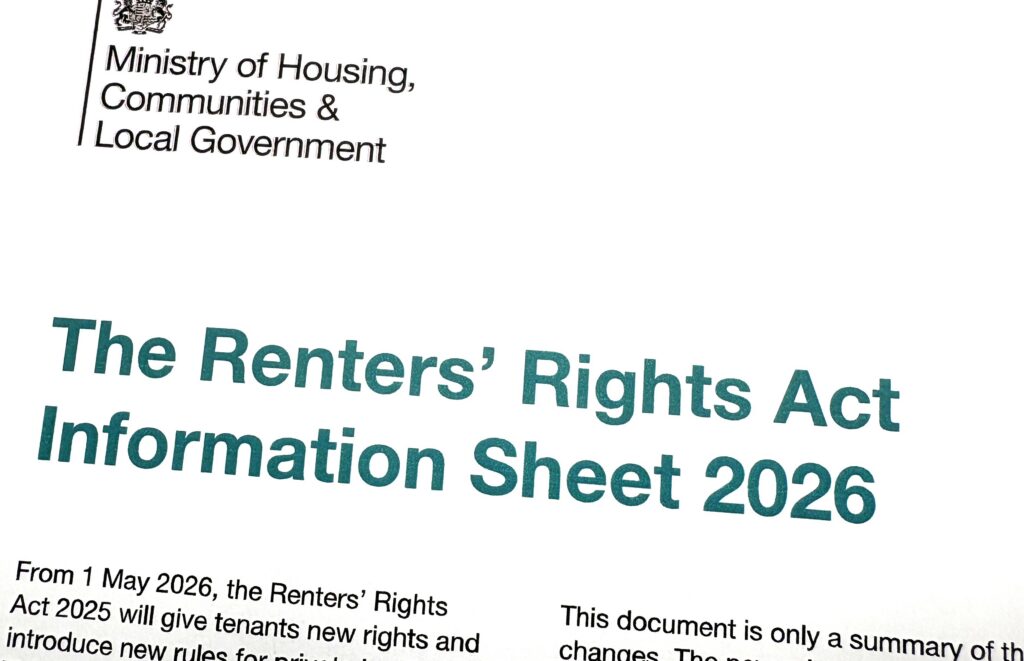

The Renters' Rights Act is now in force and there's now just a few days remaining to send the Government Information Sheet to all existing tenants.

The property rental market continues to show demand outpacing supply according to the latest RICS UK Residential Market Survey, out last week.

According to the latest figures from the Royal Institution of Chartered Surveyors (RICS), buyer enquiries and agreed sales both declined during April, with surveyors reporting weaker momentum across large parts of the country.

The number of households in England is projected to rise by 17% to 27.6 million by 2040 causing significant demographic change.

Around 5% of England’s private rental stock could be lost from the sector by the end of this year, according to projections from specialist lender Pepper Money.

The Renters’ Rights Act (RRA) is finally coming into force tomorrow and represents the most significant reset the Private Rented Sector (PRS) has seen in decades.

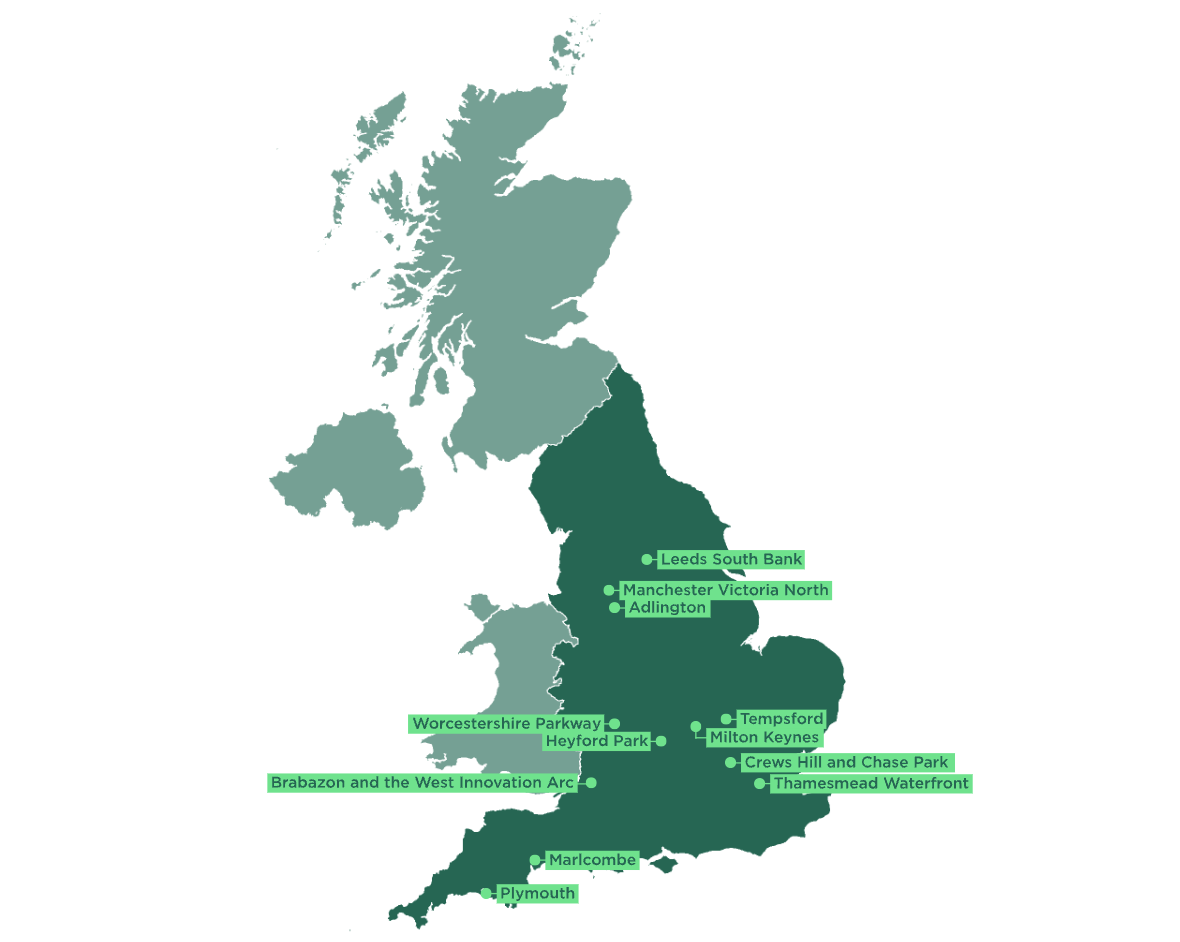

Speaking on Radio 4’s Today programme recently, the housing and planning minister Matthew Pennycook confirmed that the number of proposed sites has been reduced.

- Up To One Million Homes In England Are Vacant

- Government Releases Details For New Tenancy Agreements

- Ditch Politicians Now - Let Property Experts Run National Housing Policy

- New Data Shows Landlords Are Still Investing

- Build To Rent News

- Government Releases Renters Rights Act Information Sheet

- The Middle East War Is Affecting The Property Market

- John Lewis Pulls Out of Build to Rent Sector