We’re fast approaching the Spring selling season, which is one of the busiest periods of the year for the housing market. People emerge from winter hibernation mode to start their search for a new home, as well as lots more people listing their homes for sale.

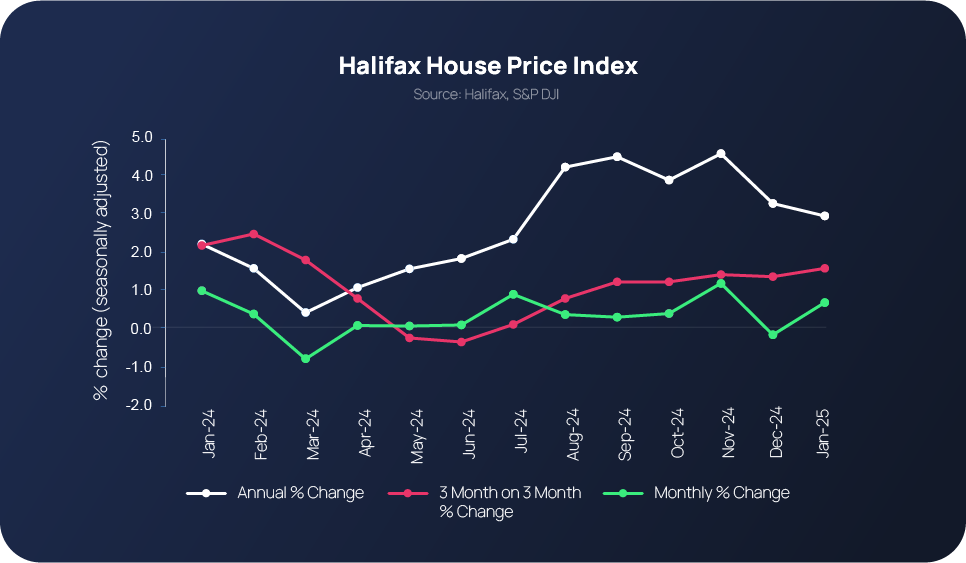

The average price of a UK property has continued to generate positive headlines after house prices soared by +0.7% January. According to Halifax’s latest House Price Index, the average property price stands at £299,138 – a new record high. This represents a monthly change of +0.7% and a quarterly change of +1.6%.

Latest figures reinforce the market’s continued resilience, which is underpinned by strong demand for mortgages and spurred on by lending growth. Overall, the outlook for this year is ‘fairly positive’, which Halifax’s Head of Mortgages, Amanda Bryden, also attributes to wider factors, including the Bank of England’s first base rate cut of the year.

The same level of positivity is echoed in Savills’ February 2025 Housing Market Update, which also highlights that overall transaction volumes increased last year (1.1 million in total), putting sales almost back in line with average pre-pandemic levels.

More than 140,000 properties were listed for sale in January, the highest number on record for a decade – data from TwentyEA has found.

The figures showed that supply was running at 7.3% higher than January 2024. This year-on-year growth was seen across all price bands, with the strongest rise of 12% seen for properties within the £350k to £1m price bracket. All UK regions saw an increase in supply with Inner London and the East Midlands leading the way with 11.3% YoY growth.

In terms of demand (sales agreed), January 2025’s volume was just under 100,000 which is the highest level seen since January 2021 and is much higher than January 2024 by 17.1%.

All UK regions saw an uplift except for Northern Ireland. The strongest growth rate was seen in the East Midlands (27.2%) and the East of England (26.8%) while all price bands benefitted, with the largest YoY growth in the £350k – £1m (28%) price bracket, followed by £200k – £350k (18%).

Katy Billany, executive director of TwentyEA, says “last year, two interest rate cuts and expectations of more to come boosted consumer confidence in the property market. Total transactions for 2024 exceeded 1.1 million, marking a 7.3% increase from 2023. The surge in supply and demand since January 2025 began, coupled with an additional rate cut, is great news for estate agents who have started the year with expanded portfolios and strong sales prospects. We believe growth in transactions will continue well into the year. While both demand and supply have increased across all property types, there are still notable nuances in the market. Houses, especially detached ones, are seeing growing popularity. The demand-to-supply ratio for this type of home has risen by 18.4% compared to the previous year, while for flats, it has decreased marginally since January 2024.”

The average original instruction price in January has fallen by 0.6% in the last year but risen by 24% since 2019. On a regional basis, instruction prices continued their 2024 trend and increased in the North and Midlands, while prices in the south were static or falling.

The North East had the largest instruction price increase year on year (9.9%) while Inner London was the only region to see year on year prices fall by more than 1% (-13.9%).

Price reductions on advertised properties were a key feature of the property market in 2024 and this trend has continued into 2025. In January alone there were more than 93,000 price reductions – the largest amount on record – however this was most likely related to the increased volume of supply. In January 2025, 36.6% of concluded listings had at least one price reduction but in January, this was slightly higher at 38.5%.

Billany adds: “Compared with last year, the price reduction rate in January 2025 reduced in all price bands and in all regions (except for Wales) which is possibly a sign that some sellers are becoming more realistic and accepting that mortgage costs remain high.”

The time to sell in January 2025 increased to an average of 90 days which is the longest period observed in the last six years and 7.6% higher than January 2024 when it was 83 days. Every price bracket has been affected and on average, it now takes 127 days to sell a property for £1m+.

Most UK regions except for Northern Ireland and the North East, have seen the time to sell increase. The South East observed the largest YoY increase of 14% (+11 days).

North-South divide presents opportunities for buyers

A new analysis by a prominent buying agent suggests the housing market is strong but showing a growing north-south divide – with London providing particularly good value for money right now.

British house prices increased by 4.6% in 2024 after a 3.9% increase in the 12 months to November, the Office for National Statistics says.

In England the December data shows, on average, house prices have not changed over the previous month. The annual price rise of 4.3% takes the average property value to £291,000.

The regional data for England indicates that the East of England experienced the most significant monthly increase with a movement of 0.6%; Yorkshire and the Humber saw the greatest monthly price fall, with a drop of -0.8%; while the North East experienced the greatest annual price rise, up by 6.7%.

However, London says now price change at all. Indeed, on average house prices in the capital decreased by 0.3% since November 2024 meaning the average price of a property is £549,000.

Jonathan Hopper, chief executive of Garrington Property Finders, says: “Not since the heady post-lockdown ‘race for space’ has the divergence between London prices and the rest of the UK been so stark. Average property prices in the capital ended 2024 exactly where they began the year. Zero growth over the year as a whole, and we even saw London prices fall in November and December. This is partly a whiplash effect from the tax rises announced in the Chancellor’s October Budget, which hit sentiment hard at the top end of the market. Buyers in the capital have since become highly price-sensitive, and willing to negotiate hard on price or simply look elsewhere.

At the other end of the scale, the market dynamics in Scotland and Northern Ireland are seemingly detached from economic gravity. Two factors underpin their rapid price growth – soaring rent increases have nudged many tenants into buying their first home, and the relatively strong value offered in both nations compared to other parts of the UK has lured price-conscious buyers from elsewhere. That second factor also lies behind the brisk pace of price rises across Northern England, and continues to widen the North-South divide.

The property market is broadly in good health. The supply of homes for sale is strong and the cost of borrowing has edged down in February – with lenders offering mortgage interest rates below 4% for the first time in months. The number of homes for sale is so abundant in some areas – even in highly sought-after, prime postcodes – that buyers find themselves firmly in the driving seat and able to drive a hard bargain on price. This is likely to keep future price rises modest in much of southern England, and anyone planning to put their home on the market there in the coming months will need to price it competitively to attract buyers.”

Wales shows, on average, house prices fell by 0.5% since November. An annual price increase of 3% takes the average property value to £208,000.

Separate statistics show that in December 2024, on a seasonally adjusted basis, the estimated number of transactions of residential properties with a value of £40,000 or greater was 96,000. This is 18.7% higher than in December 2023. Between November 2024 and December 2024, UK transactions increased by 2.9% on a seasonally adjusted basis.

The North-South divide and the plight of London’s market are all echoed in the latest data from the respected asking price index produced by the Home website.

It says sellers across Greater London and the South of England are resorting to competitive pricing due to high stock levels.

Contrary to seasonal expectations, the mix-adjusted national average asking price has dipped early this year, driven by significantly lower pricing in the capital as well as the South East and South West of England.

In stark contrast, vendors in the North and Scotland are much more confident in their pricing. Among these top performing regions, Yorkshire indicated the largest monthly rise of 0.8%, seemingly a world apart from the pain felt in the South.

The Northern Powerhouse city of Manchester has come out on top as an investment destination in England for the second time.

The latest ‘Top UK Residential Investment Cities‘ report for H2 2024 from Colliers has revealed the 20 best-performing cities across the UK by focusing on five key pillars: economic, research and development, liveability/cultural, property and environmental.

The analysis is designed to help investors to make “informed capital allocation decisions”, according to Colliers director of research and economics, Oliver Kolodseike, with the latest report being the eighth in the series.

At the top of the table UK-wide are Scottish powerhouse cities Edinburgh and Glasgow; a position they have now held for three consecutive reports, which are released twice a year.

Ranked third overall, but in first place for England, the North West city of Manchester retains its status for the second report in a row – which its highest placing since Colliers’ analysis began, demonstrating the improvements across the city that make it a promising hotspot for residential investors.

Hailed in particular for its thriving economy, R&D credentials, exciting jobs market and booming population, Manchester is proving particularly popular among investors seeking a more affordable location than London, with exciting future prospects.

Manchester is “world-class”

The report notes: “Manchester continues to be a world-class city region, offering a fantastic environment for living in and for businesses to grow and prosper.

“Home to an £80 billion economy, global transport connectivity, incredible talent from the largest student population outside of London and high-quality business properties, it is a first choice investment destination for leading international brands.”

Office take-up has experienced a steep rise over the past year, hitting its highest figure since pre-pandemic in 2024 with a total of 1.22m sq ft transacted, according to Colliers, which is higher than the city’s five-year average. One of last year’s most significant office transactions was BNY Mellon’s acquisition of 200,000 sq ft of space in the city centre.

This follows on from a number of large corporations and government bodies relocating to Manchester over the past five years. These include JP Morgan, Octopus Energy, and Rolls Royce.

These moves have boosted employment while also increasing demand for homes, which has further enhanced the city’s investability in the residential sector, and boosted property prices at the same time, with Manchester recording the second-highest house price growth of the 20 cities analysed for the report. It also has a high share of properties with an EPC rating of A-C.

The report adds “Culture, art, music, sport and festivals are in abundance and this combined with easy accessibility to the surrounding beautiful countryside of the Peak District, Lake District and North Wales offer a compelling reason to live and work here.”

Strong economic outlook

In Colliers’ H1 2024 report, Manchester was ranked at the top of the 20 cities for its economy. In this report, it falls to third position, although it holds the second-best GDP forecasts of all cities analysed.

Manchester’s economy is forecast to grow at an annual rate of 2.2% over the next five years, says Colliers, while the unemployment rate is forecast to average 3.7% over the same period.

The city’s population is also forecast to see the highest growth of any of the 20 cities, with a projected increase of 1.07% per year over the next 10 years.

Another area where Manchester scored particularly strongly was in the R&D measurements, where the cities remains in fifth position due to its “positive net business creation”.

“Furthermore, Manchester benefits from the second largest student population and its university ranks 22nd in the 2025 University League Table,” adds the report.

UK housing market needs long-term observation

Andrew White, head of UK residential and international properties, Asia, said “the housing market has been in a holding pattern in recent years, which is broadly reflected in our latest analysis with our top four cities remaining in the same position. However 2025 could be the year where that changes. We’re expecting a flurry of activity in the first quarter with the stamp-duty threshold reducing for first time buyers, also the cost of borrowing should start to come down as the Bank of England is expected to continue to reduce the base rate this year, and with unemployment remaining low, perhaps for some homeownership will become more viable.

What will be interesting to note this year is whether the affordability gap between the locations we analysis will shrink, and whether the demographics of our regions and cities could be altering – although that is more likely to require a longer term observation, it is one for the Government to be mindful of.”