Property – it’s one of Britain’s best-loved investments. A pension plan for many, it provides the benefit of regular rental income, as well as capital growth in the long run, providing an ultimate pay-off after years of monthly payments when sold.

But like any financial asset, it carries risk.

You need to factor in costs such as maintenance, repairs, insurance, tax and other fees – as well as void periods.

Buy-to-let investors also need to be aware that recent changes to the tax rules, along with a stamp duty surcharge on the purchase of additional homes, and new legislation on the energy efficiency of newly let properties, could all push up costs – not to mention add extra red tape. That said, if you take a long-term view of buy-to-let, you can make it work for you. When it comes to purchasing a rental property, unless you are lucky enough to have the cash to buy outright, you will need a type of mortgage known as a buy-to-let.

Here, we take a closer look at the ins and outs of this type of deal.

How do buy-to-let mortgages work?

A buy-to-let mortgage is a way to purchase a property you plan to let out, as opposed to living in yourself.

Most are interest-only, meaning you only pay the interest each month, but not the capital amount – and pay off the mortgage balance at the end of the term. While deals are also available on a repayment basis, landlords typically opt for interest-only, as the monthly payments are a lot lower – increasing their overall cash flow.

But if you do decide to go for interest-only, you must have a viable repayment plan in place and understand the risks involved.

Should I register as a limited company?

In recent years, there has been a rise in the number of people registering as “limited liability companies” to purchase buy-to-let properties. This move has been prompted by changes to the tax rules (and specifically the mortgage tax relief rules). For some, starting a limited company may provide a more favourable taxation scenario, but this is not the case for everyone – so make sure you’ve done your research.

Who can apply for a buy-to-let mortgage?

Generally speaking, someone purchasing a buy-to-let already owns a place which they live in themselves, though it is possible to buy an investment property if you are a first-time buyer.

Marylen Edwards, head of buy-to-let at MT Finance, a lender, said “anyone has the ability to apply for one of these mortgages, subject to passing the lender’s due diligence checks and the property being suitable at valuation stage. For example, we accept applications from individuals, limited companies, first timers, first-time landlords and more.”

Age limits may apply. Jonathan Samuels, of property finance firm Octane Capital, said “most lenders require you to be at least 21, though some will consider applications from those aged 18 or above. At the other end of the scale, most buy-to-let lenders won’t lend beyond age 75.”

Lenders use a rental affordability calculation to determine how much you can borrow, and whether they think your buy-to-let mortgage is viable.

Nick Mendes, of mortgage broker John Charcol, said “when assessing your affordability, buy-to-let lenders will base your loan on the expected rental income of the property. Some lenders can take personal income into account as well, to support the application. This is called ‘top-slicing’. Lenders assess affordability by comparing gross rental incomes with interest payments via a measure called the 'interest coverage ratio', or 'ICR'. Banks usually require a minimum ICR of 125% or limited companies and basic-rate taxpayers, rising to 145% for higher-rate taxpayers.”

Buy-to-let mortgages typically require a minimum deposit of 25%. The larger your deposit, the greater the range of mortgage products you can choose from and, usually, the cheaper the rate.

Howard Levy, director of mortgage broker SPF Private Clients, said “purchases via limited companies qualify for more sympathetic stress tests and therefore potentially higher loan amounts, due to the more favourable taxation rules.”

Where can you get a buy-to-let mortgage?

There are currently around 1,500 buy-to-let products offered by a mix of high street lenders, building societies and specialist lenders. While many will allow you to approach directly as a customer, several lenders will only offer their products through an intermediary, such as a broker.

When looking for a buy-to-let, as with any type of mortgage, it makes sense to speak to a broker, to help you get the deal best suited to your needs.

Choosing a buy-to-let mortgage

When making your choice, there are many different things to consider.

As mentioned above, you need to choose between interest-only and repayment; you then need to make a decision between fixed rates, trackers, discount rates and so on. Mr Levy said “choosing a buy-to-let can be a minefield, as it’s not as simple as opting for the lowest rate. Each lender has specific criteria that need to be adhered to. Other things to think about include whether you are buying in your own name, or a limited company, the rent achievable from the property, and how many properties you already own.”

How to apply for a buy-to-let mortgage

You can apply for one of these deals either directly or via a broker. Given buy-to-lets can be quite complex, especially if you’re a new landlord, there may be a lot of benefits to using a broker.

They will, for example, know the particular requirements for each lender and will look at your entire situation and needs and advise you accordingly. A broker will also guide you through the process, ensuring you understand how buy-to-let mortgages work and exactly what you’re applying for.

How tax is applied with buy-to-let

With buy-to-let, there are different forms of tax to consider. The main three are stamp duty, capital gains tax and income tax. These are paid at different times.

*Stamp duty

This tax is paid on the initial purchase.

When you acquire a second home or a buy-to-let property, you’ll pay stamp duty at the standard rates, plus a 3% surcharge on each band.

Stamp duty

© Provided by The Telegraph

*Capital gains tax

You pay capital gains tax on the portion of the profit you earn from the sale of a buy-to-let property. The amount you pay depends on your personal income and the profit you get from the sale. You can deduct certain costs from taxable gains to reduce the tax you pay, such as stamp duty, estate agent fees, solicitor fees and costs for improvements to the property.

For the 2023-24 tax year, the tax-free allowance for gains is £6,000, down from £12,300 previously. This means you don’t pay any tax on the first £6,000 you earn from the sale of your property. You don’t pay capital gains tax on property owned and sold by a limited company. You pay corporation tax. This currently stands at 25%. This is because any property you own is viewed as part of your business, not a personal investment.

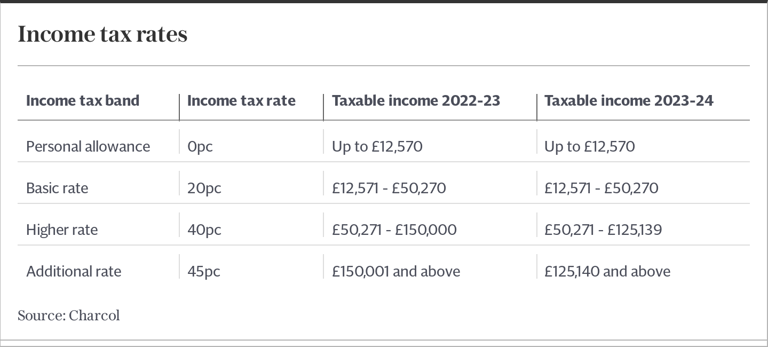

*Income tax

Your income tax band determines the rate at which you’ll pay tax on rental income that year. The income tax rates and thresholds for your rental income are the same as those for your personal income. However, adding your net rental income to any other income you receive may push you over your usual tax threshold and into a new, higher band.

income tax

© Provided by The Telegraph

Note that if you earn less than £1,000 a year in rental income, you do not have to report it to the taxman. Earn more than this, and you will need to register with HM Revenue & Customs for self-assessment.

Mr Samuels said:“you will need to declare this income on your tax return, though it can be offset against a range of expenses, such as letting agent fees, maintenance costs and council tax.”

What has happened to mortgage interest relief?

Over the last few years, the Government phased out the amount of mortgage interest relief you could claim, while simultaneously introducing a new tax relief, called a “tax credit”.

Mr Mendes said “holding buy-to-let property in a limited company may offer some tax benefits to certain individuals. For example, some higher-rate taxpayers may find it to be more tax-efficient than owning property as a private landlord.”

That said, some will still be in a better tax situation if they remain without one.