The latest data from Nationwide has revealed that house prices took a tumble in October 2022, falling 0.9% month-on-month in the wake of former prime minister Liz Truss' mini budget. This is the first such fall since July 2021 and the largest since June 2020, the figures show. The average house price has also fallen from a UK average of £272,259 in September 2022 to £268,282 in October 2022.

Nationwide's Chief Economist Robert Gardner said the property market has been impacted by the mini-Budget which led to a sharp increase in interest rates, meaning housing affordability has been "stretched" at a time when "household finances are already under pressure from high inflation."

He explained that "the increase in mortgage rates meant that a prospective first-time buyer (FTB) earning the average wage and looking to buy a typical FTB home with a 20% deposit would see their monthly mortgage payment rise from c.34% of take-home pay to c.45%, based on an average mortgage rate of 5.5%."

Mr Gardner warned: "Inflation will remain high for some time yet and Bank Rate is likely to rise further as the Bank of England seeks to ensure demand in the economy slows to relieve domestic price pressures. The outlook is extremely uncertain, and much will depend on how the broader economy performs."

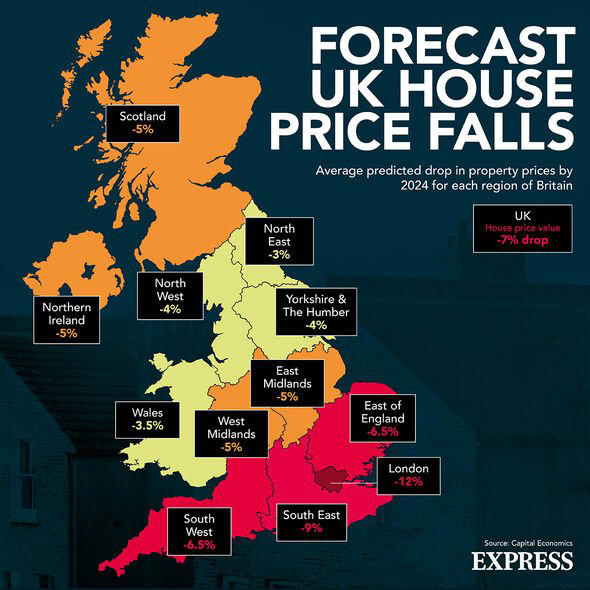

You can see from the chart below how the average house price has changed over the last two years. But as the latest data reports a decline, what does this mean for you? We spoke to the experts to find out.

Will there be a housing market crash?

James Forrester, Managing Director of Barrows and Forrester, agreed and said despite there being "panic" in recent weeks, there "remains a far greater appetite for homeownership than the available housing stock to satisfy it."

"While this remains the case, any fears of a property market crash can be firmly put to bed and we expect to see house prices continue to increase on an annual basis throughout the remainder of the year, albeit at a more measured pace, as has already been the case in recent months."

Is now a good time to buy a house or not?

Asked if now was a good opportunity for some, Jonathan Rolande, founder of property firm House Buy Fast, said: "Well, the market is still at an almost all-time high so sellers can cash in and sell now - and there are still plenty of buyers about. But only sellers who aren't re-buying or are moving down market will benefit.

"Many buyers have been waiting for a downturn as an opportunity to buy and save money. This isn't it. With banks tightening lending and rates through the roof, it is more expensive to buy with a mortgage now than it was a year ago, even taking into account the drop in prices.

"The shockwaves of the budget have now passed but we must expect difficult trading conditions as the cost of living rises truly begin to bite this winter."

Nathan Emerson, Chief Executive of Propertymark, the UK professional body for estate agents, said agents are also reporting more homes for sale which is giving buyers more choice compared to the last two years.

He added: "They no longer have a fear of losing out on a property and can therefore be more level-headed with the offers they're putting forward, which will naturally see a softening in prices being achieved over the next few months."

David Hollingworth of L&C Mortgages said it was "no surprise to see aspiring buyers and sellers taking a wait-and-see approach" following the turmoil in the wake of the mini budget, adding that this could help buyers have more bargaining power.

He said: "First time buyers may hope that availability and pricing of property will improve as they consider the impact of higher mortgage rates on their position. Ultimately if the right property can be found for the right price then it could still be the right time to buy and the volatility of just a month ago has subsided which will make it easier for buyers to take stock in the coming weeks and months.

Matt Hoy, Managing Director - Residential at Bradley Hall, said: "Last month marking the first time that house prices have fallen since July last year, when the final lockdown measures were eventually lifted, shows just how much impact the recent economic changes have had on the UK's housing market.

"Already stretched by rising household bills caused by the sharp rise in inflation, the cost increase of borrowing for a mortgage has further strained the market, with even less people now able to afford a home despite the nation being in the midst of a chronic housing shortage.

"Nevertheless, there are still reasons to be optimistic. The changing of the guard of government with the appointment of a new Prime Minister and Chancellor has led to borrowing costs falling back somewhat in recent weeks and this could continue as the pound bounces back in value and business confidence restores.

"There will undoubtedly be bumps along the road, and the recovery may not immediate, but with unemployment at a 50-year low and plans afoot to push through planning reform and unlocking more housing developments across the country, we will hopefully see the market bounce back sooner rather than later."

The competition for homes is high - but there is more choice

Despite a sharp slowdown in annual house price growth, property experts and agents are still reporting a surge in enquiries, with Matthew Thompson, Head of Sales at Chestertons, saying their branches registered the same volume as October 2021.

He said: "October's property market was very much dictated by the avalanche effect of September's Mini-Budget announcement. Buyers were facing the reality of higher interest rates and mortgage providers withdrawing a number of products, which created a new sense of urgency.

"This has led to house hunters rushing to finalise their purchase, resulting in a 53% increase in the number of exchanges compared to October last year."

However, while the competition to secure your next - or first - home may be fierce, experts say we are seeing more houses come onto the market compared to the last two years.

Nathan Emerson, Chief Executive of Propertymark, said: "[Buyers] no longer have a fear of losing out on a property and can therefore be more level-headed with the offers they're putting forward, which will naturally see a softening in prices being achieved over the next few months."

More sales falling through

Data from House Buyer Bureau shows that the number of property sales falling through has increased for the first time since the height of the pandemic market boom.

The number of property sales falling through has increased for the first time since the height of the pandemic market boom at an average cost of more than £3,000 for those involved, new research claims.

Analysis by ‘quick buy’ firm the House Buyer Bureau, using TwentyCi data, has tracked the number of transaction fall throughs across the UK property market and how much this costs for buyers and sellers in the transaction.

The research found that some 78,042 sales are estimated to have been subject to a fall through during the second quarter of this year.

This marks a 9% increase versus the previous quarter and the first quarterly increase since a market peak of 87,817 in the second quarter of last year.

The level of fall throughs remains down 11% annually versus the peak seen in the second quarter of 2021, according to the research.

But while fall through volumes are still down on the previous pandemic market peak, the average cost of a fall through has climbed to a record high.

The latest figures show that the average fall-through now costs those involved £3,209 per a transaction – a 2% increase on the previous quarter and a 9% annual jump.

As a result, the total cost of transaction fall- throughs, including fees already paid such as conveyancing and surveys, to the UK property market exceeded £250m in the second quarter of this year alone.

The figure is 11.2% more than the first quarter of the year, with the total cost of fall throughs in 2022 so far alone hitting almost £476m.

In 2021, this total market cost hit over £1bn, the highest annual cost to the market in the last four years, with 2022 looking likely to come close, if not exceed this threshold.

Chris Hodgkinson, managing director of the House Buyer Bureau, said the cost of fall-throughs in 2021 was more than £1bn and said this year could come close or even exceed that figure.

He said: “Property sale fall-throughs are simply an unfortunate reality of a property market that affords very little protection to buyers and sellers right up until a sale has actually completed.

“While it’s the buyer that often gets hit by the majority of the cost, both parties can see their hard-earned cash go to waste due to a fall through, having paid out for costs such as conveyancing fees, with many sellers also hit if their own onward purchase is jeopardised.

“Unfortunately, we saw the level of fall throughs plaguing the market hit new highs during the manic frenzy of the pandemic property boom. This was largely down to an increased number of transactions in general, coupled with a market that was swamped with buyers fighting it out for limited stock, with the practice of gazumping becoming particularly prevalent.

“While the volume of fall throughs had been in slow decline, they’ve started to climb once again in 2022.”

He suggested the driving factors behind fall-throughs in the current market are different and include spiralling mortgage rates.

| Quarter/Year |

Est number of fall throughs |

Est average cost of fall through |

Est total cost of fall throughs to property market |

Est total cost of fall throughs to property market by year/quarter |

| Q1 2018 | 50,000 | £2,700 | £135,000,000 | £588,600,000 |

| Q2 2018 | 58,000 | £2,700 | £156,600,000 | |

| Q3 2018 | 59,000 | £2,700 | £159,300,000 | |

| Q4 2018 | 51,000 | £2,700 | £137,700,000 | |

| Q1 2019 | 60,491 | £2,738 | £165,624,358 | £765,617,475 |

| Q2 2019 | 71,555 | £2,738 | £195,917,590 | |

| Q3 2019 | 76,793 | £2,738 | £210,259,234 | |

| Q4 2019 | 70,788 | £2,738 | £193,816,293 | |

| Q1 2020 | 66,602 | £2,788 | £185,686,376 | £832,719,840 |

| Q2 2020 | 77,359 | £2,788 | £215,677,821 | |

| Q3 2020 | 77,359 | £2,788 | £215,677,821 | |

| Q4 2020 | 77,359 | £2,788 | £215,677,821 | |

| Q1 2021 | 86,375 | £2,951 | £254,892,625 | £1,011,537,140 |

| Q2 2021 | 87,817 | £2,951 | £259,147,967 | |

| Q3 2021 | 87,063 | £2,951 | £256,922,913 | |

| Q4 2021 | 81,523 | £2,951 | £240,573,635 | |

| Q1 2022 | 71,613 | £3,146 | £225,294,498 | £475,731,276 |

| Q2 2022 | 78,042 | £3,209 | £250,436,778 | |

| Q change % | 9.0% | 2.0% | 11.2% | 11.2% |

| Annual change % | -11.1% | 8.7% | -3.4% | -3.4% |

Est average cost of fall through based on source value and vs house price, as well as estimated according to inflation increases and legal fee increases